LEAVE ENCASHMENT AT THE TIME OF SUPERANNUATION FULLY EXEMPTED FROM INCOME TAX W.E.F. 01.03.2018 FOR RETIREES RETIRED DURING 2018-19. WE OFFER OUR SINCERE THANKS TO SHRI M C GUPTA RETIRED SR. ENGINEER FROM SARAS DAIRY. MR I M AGRAWAL EX CM PNB FOR THEIR RELENTLESS EFFORTS WHO WAS TRYING HARD TO GET THE ANOMALY ADDRESSED BY CBDT. THE MESSAGE RECEIVED IS POSTED BELOW.

Good News for those retiree’s who retired in financial year 2018-19 and afterwards. When I was filing IT return I noticed that IT department has exempted income earned by way of earned leave encashment under Section 10 (10aa) which can be claimed under column:

Less:Allowances to the extent exempt u/S 10 under sub section 10 aa. All members retired in f/y 2018-2019 are advised to note it down and claim exemption under Leave Encashment. Regarding previously retired employees can claim it after filing revised return under the guidance of CA.

Regards

I M Agrawal

Friends, who are retired after April,2018 they are eligible for exemption of IT section (10) sub section (10aa) under this section, your leave encashment is fully exempted & no tax is to paid, so if you have already deducted tax for leave encashment above 3.00 lacs can be refunded to you. Take care while filing return.

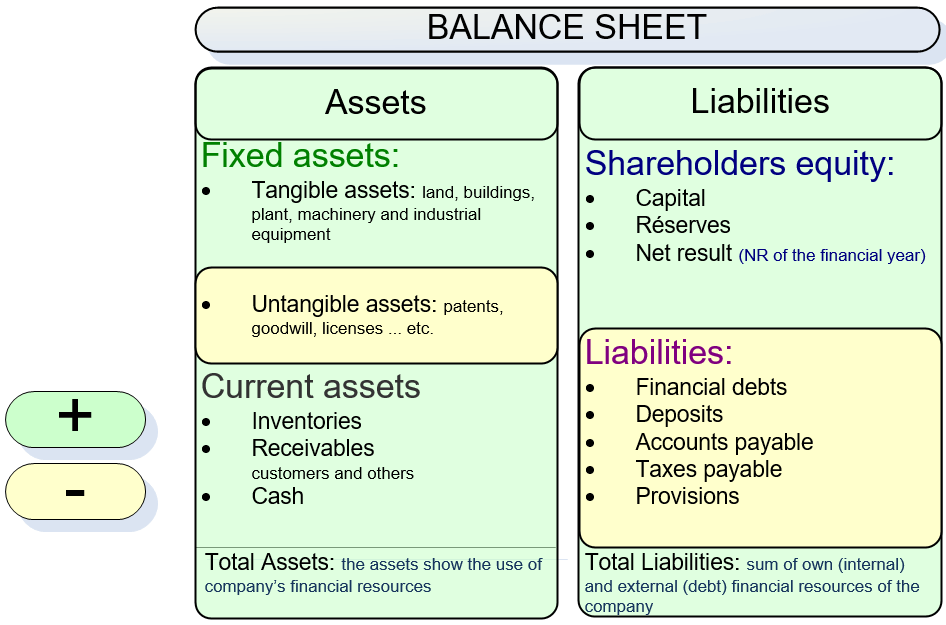

Total liabilities / total equity: It’s showing the proportion between equities (internal financing) and debts (external financing). The more important the internal financing is, the lower is the risk of bankruptcy.

Total liabilities / total equity: It’s showing the proportion between equities (internal financing) and debts (external financing). The more important the internal financing is, the lower is the risk of bankruptcy. Should not exceed "1" in which case the banking dependence level is too high.

Should not exceed "1" in which case the banking dependence level is too high. In order to perform a relevant solvency analysis it is needed to detect this falsifications which can skew the assessment and the analysis which results from this.

In order to perform a relevant solvency analysis it is needed to detect this falsifications which can skew the assessment and the analysis which results from this. The principle of tangible net worth is not to deny the intangible assets of a company which are, in most cases, a reality, but to put them aside because they do not help the company meet its debts .

The principle of tangible net worth is not to deny the intangible assets of a company which are, in most cases, a reality, but to put them aside because they do not help the company meet its debts .